Importance of the Debt to Assets Ratio

The debt to assets ratio measures how much of a nonprofit’s resources are financed by debt rather than by net assets. It provides insight into leverage and long-term risk. While some borrowing can be strategic (acquiring property or bridge funding gaps), excessive debt can compromise flexibility and increase financial vulnerability. For nonprofits in social innovation and international development, where funding cycles are uncertain and revenue can be restricted, this ratio helps boards and donors assess whether the organization is relying too heavily on debt to sustain operations.

Definition and Features

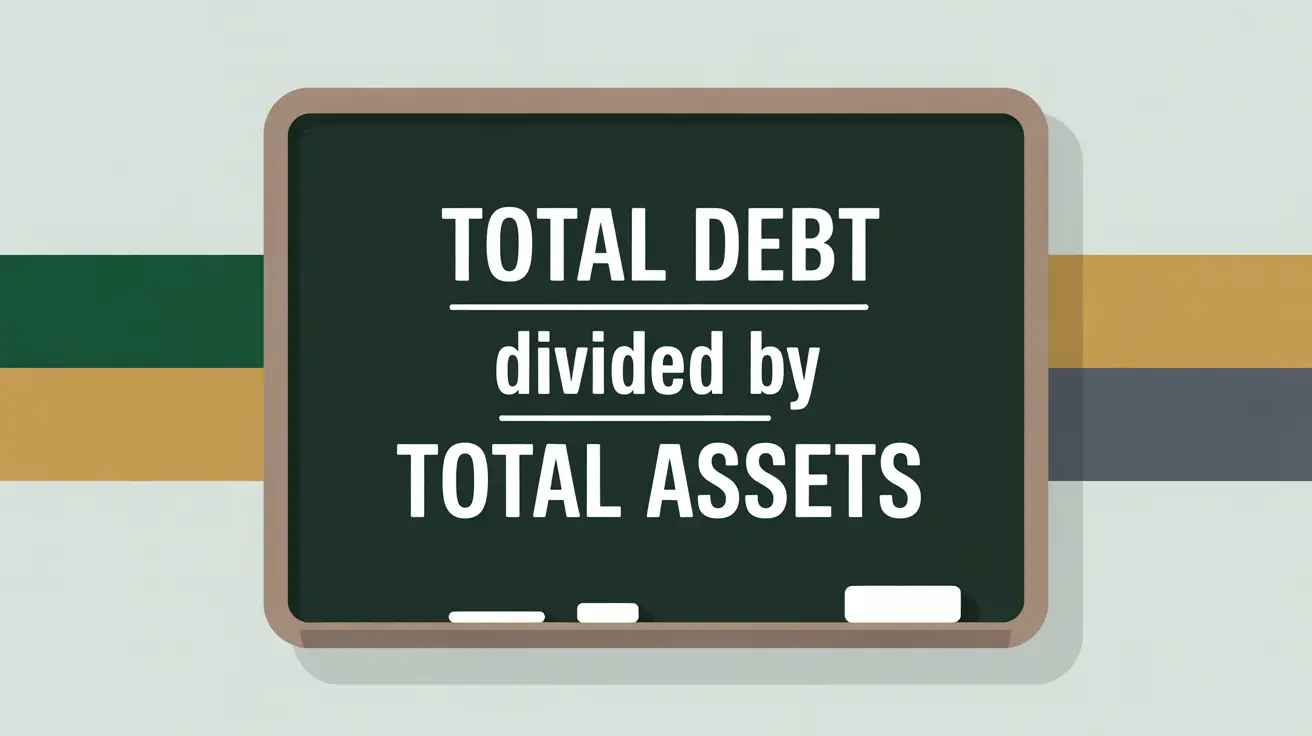

The debt to assets ratio is defined as:

Total Debt divided by Total Assets.

Key features include:

- Leverage Indicator: shows what portion of assets is financed through debt.

- Risk Benchmark: higher ratios indicate greater reliance on debt and higher financial risk.

- Decision Tool: helps boards evaluate capacity for future borrowing or expansion.

- Donor Perspective: influences perceptions of financial stability and risk tolerance.

How This Works in Practice

If a nonprofit has $3 million in total debt and $12 million in total assets, its debt to assets ratio is 0.25, meaning 25% of its assets are financed by debt. This may be seen as a prudent level of leverage. A ratio above 0.5, however, might raise concerns about financial risk, especially if the nonprofit depends on uncertain donor flows to cover debt service. Finance committees often review this ratio before approving loans, bond issues, or capital campaigns that involve borrowing.

Implications for Social Innovation

For nonprofits in social innovation and international development, the debt to assets ratio is an important governance and donor confidence measure. Organizations working across borders often face cash flow delays and may be tempted to borrow for continuity. A manageable ratio signals that debt is used strategically without jeopardizing long-term solvency. Conversely, a high ratio may erode donor trust, especially if liabilities outpace unrestricted reserves. By tracking this measure, nonprofits can make informed decisions about when to borrow, how much leverage is prudent, and how to balance growth ambitions with financial sustainability.